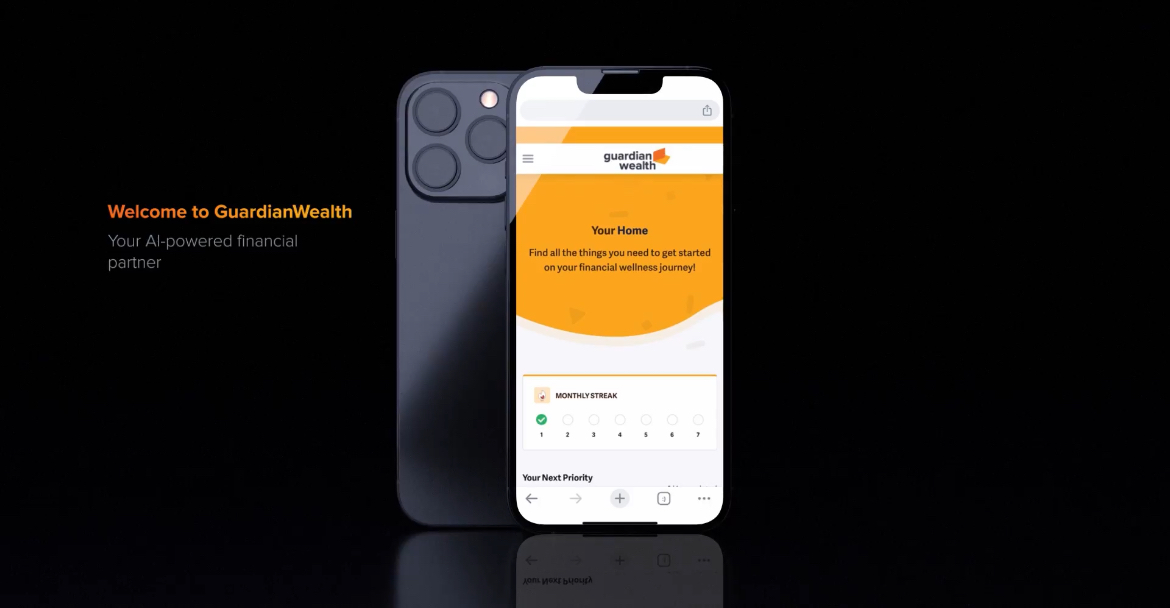

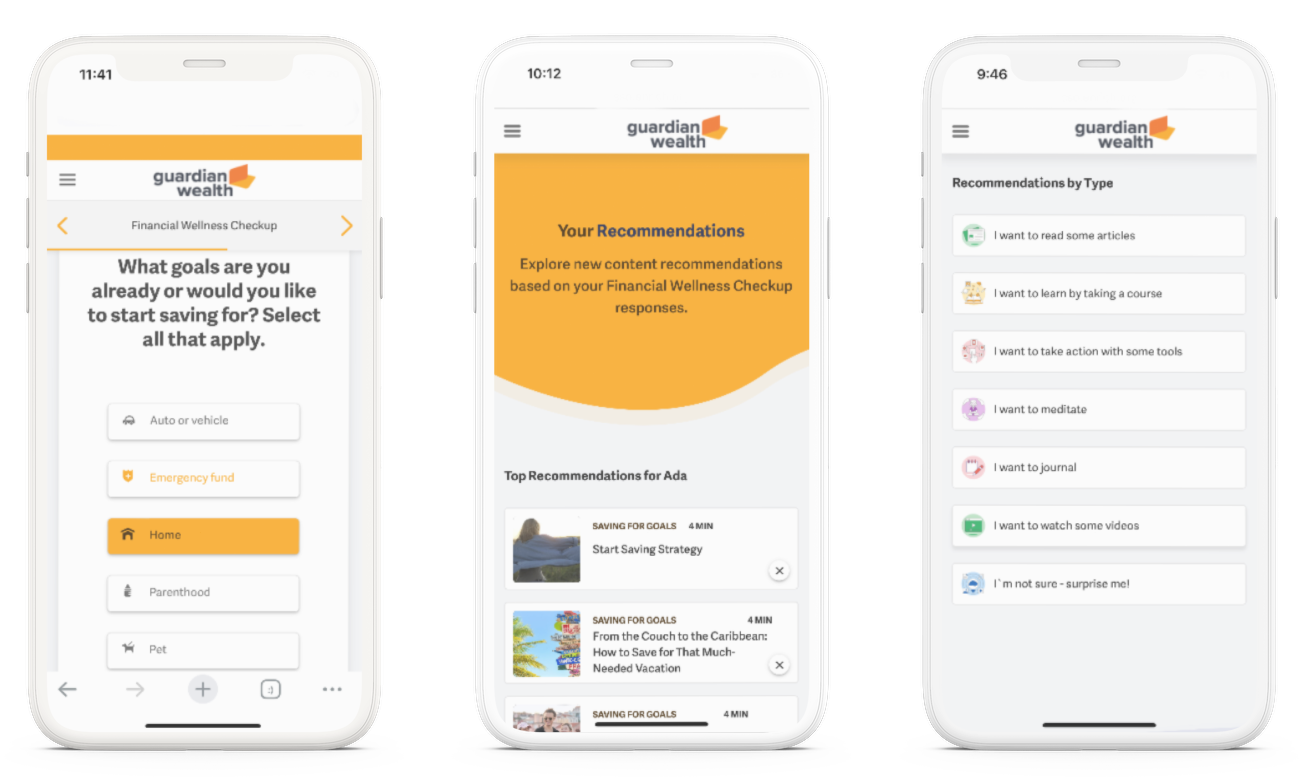

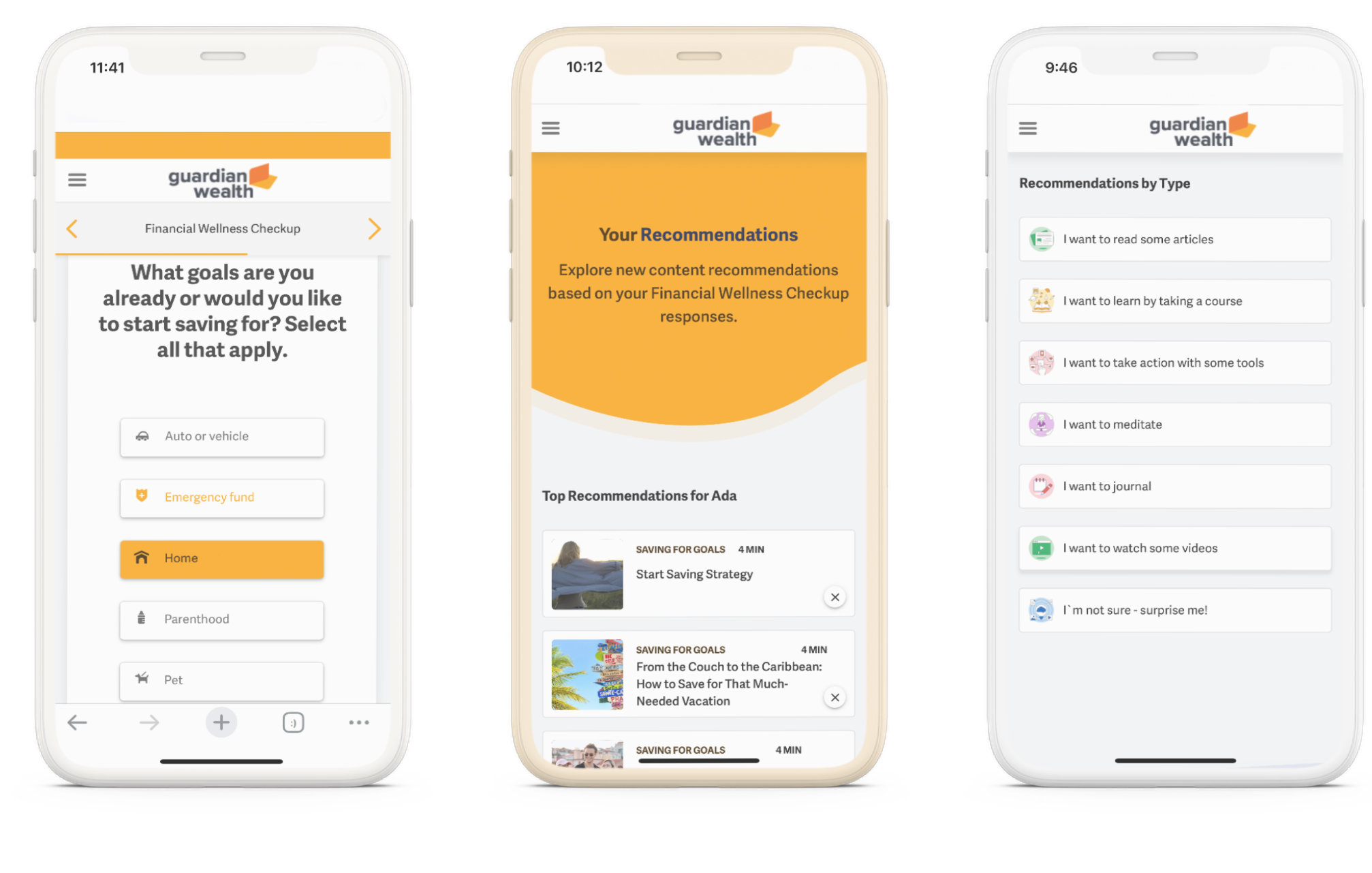

Built by financial experts, our AI-powered platform empowers you to take control of your financial future.

Start with a financial health checkup — in less than 5 minutes — get your personalized recommendations with tools, content, and courses that are right for you.

We make direct ownership in US real estate accessible and transparent. With a stable market, attractive rental yields, and a history of long-term appreciation, the U.S. offers a solid foundation for your investment portfolio.

Our expert team will be your trusted guide every step of the way from buying to property management, and even selling when the time is right. Discover the potential of US real estate to build wealth.

As a Nigerian family, we always dreamed of investing in the US real estate market but didn't know where to start. GuardianWealth made our dream a reality. They guided us through every step, from choosing the right property to securing financing. Now, we're proud owners of a property in the US, and it's a significant step in safeguarding our wealth against currency devaluation.

GuardianWealth transformed the way I manage my finances. It's like having a personal financial advisor in my pocket!

I thought owning property in the US was out of reach for me, but GuardianWealth changed that. Their expertise in accessing financing options opened doors I didn't even know existed. Thanks to their support, I'm now a property owner in the US, which has been a game-changer in my wealth-building journey.

What I love about GuardianWealth is its adaptability. It's grown with me as my life situation has changed. It's like having a financial friend for life.

Investing in US property with my friends seemed complex, but GuardianWealth simplified the process. Their team provided invaluable advice and support, allowing us to pool our resources confidently. This investment has not only been financially rewarding but has also brought us closer together.

The Financial Health Checkup was eye-opening. I realized where I was overspending and got practical tips to improve my financial health.

The recommended courses and articles are spot-on. I've learned so much about investing and growing my wealth.

Mindful Meditation has been a game-changer for me. It's not just about money; it's about a healthier relationship with it.

GuardianWealth isn't just about buying property; it's about building lasting wealth. Their insights into the US market and understanding of the Nigerian perspective have been instrumental in my financial growth. I've not only hedged against devaluation but also set a foundation for future generations.

The path to wealth creation can be fraught with challenges. You don’t have to go it alone. Invite friends, make new friends and be empowered. Be part of a community of Wealthbuilders.

As we navigate the digital age, the landscape of personal finance is undergoing a profound transformation. No longer are we...

Read MoreObtaining a conventional mortgage can be a complex and time-consuming process, often involving a mountain of paperwork. The documentation typically...

Read MoreAcross the spectrum of investment avenues, real estate stands out as a consistent, tangible, and historically rewarding asset class. It’s...

Read More